CapitalTime

Articles on investing and capital management, with a quantitative focus.

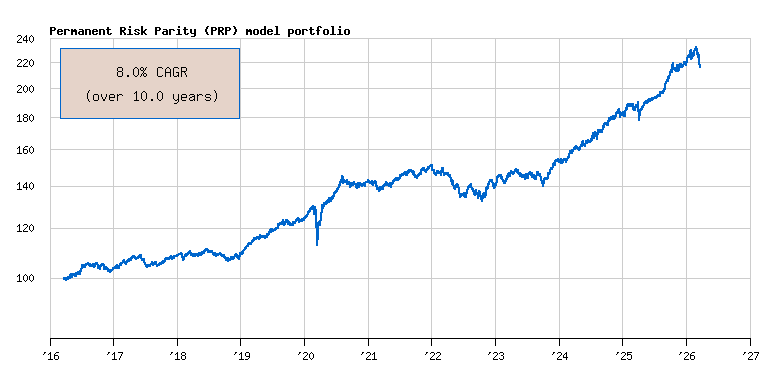

10 Years of Permanent Risk Parity

2026-03-22

I started using my Permanent Risk Parity (PRP) portfolio exactly 10 years ago. It has returned 8.0% CAGR and 5.2% real return over this full period.

I’m very happy with this performance, though I expect the real return to weaken a bit going forward, as explained below.

Note: I am not a financial professional or an advisor. This web site documents my investing experience and is not advice. You should not use my portfolio.

Performance

The calculations below show the compound annual growth rate

(CAGR) in both nominal, and real (inflation-adjusted) terms. I’m

comparing my portfolio to XBAL, a low-fee 60/40

balanced ETF which has some of the same holdings.

Remember that the real return is what really matters. The goal of investing is to preserve and hopefully increase the purchasing power of money.

To calculate real returns, I used a 2.7% inflation rate (source).

| PRP | XBAL | |

|---|---|---|

| Nominal Return | 8.0% | 7.2% |

| Real Return | 5.2% | 4.4% |

PRP outperformed XBAL over the 10 years, though at

many times within this decade, I saw very comparable performance

between the two.

The long term performance (using historical data) for my asset allocation shows 7.2% CAGR nominal, which translates to 5.0% real return. More pessimistic modelling suggests that I might expect approximately 4% real return, similar to 60/40.

These are long term figures. Over shorter periods such as 3 years, or 5 years, the return could be much lower. There could even be a negative return.

The 10 year performance was very consistent with the long term history. However, I continue to expect approximately 4% real return.

The Experience

This portfolio has been a “smoother ride” than previous investment approaches I’ve tried. I’ve been comfortable in this portfolio.

I suspect that one reason I feel comfortable is that I really

like the underlying holdings. For example, I have a

long personal history with XIU going back to when I

first started trading it in the early 2000s. I also like gold

bullion as a diversifying asset. These personal tastes make PRP a

good portfolio for me, but it might be a terrible portfolio

for someone else!

Looking at the big picture, I fundamentally like having my portfolio diversified across distinct, dissimilar assets. This reduces the chance of any single asset class destroying the portfolio due to some extreme misfortune.

During stock market panics, it was reassuring to know that I had limited equity exposure. For example, when the economy halted in 2020, business earnings and GDP fell off a cliff. For a moment, it looked like the worst economic contraction since the Great Depression. At the time, stocks felt like a terrible investment, and I was happy that I only had 30% exposure (revised to 40% in recent years).

Although my portfolio had less volatility than 100% equities, I still saw volatility and some pretty wild swings; see the next section. Both 2020 and 2022 were unpleasant experiences.

After 25 years of investing, I have come to see the activity as being equal parts technical and psychological. Both are critical elements. One has to craft a sensible portfolio that contains reasonably good investments, with sufficient diversification and low fees… but that’s not all.

Investors also battle behavioural challenges and social pressures. Humans have a tendency to chase returns; panic; get disillusioned; become greedy; feel influenced by others; react to news. Some people work with an advisor, who can help with “behavioural coaching” and reassurance. On the other hand, advisors are not immune to these same forces, and they charge high fees.

Investing is both a technical and psychological game. I have found that using the PRP helps me with the psychology. For example, the extra diversification alleviates my concern about being overly exposed to any single asset class (a core benefit of risk parity). The dampened volatility makes markets more tolerable, much of the time.

Finally, the passive indexing approach – only using major benchmark indices with no active management – eliminates concerns about active managers and timing the market. I find that I now just accept what happens in the markets, and there is a kind of serenity to this. I simply don’t know what the market will do, and that’s fine. Nobody knows what the market will do. We’re just along for the ride.

To achieve the long-term CAGR of markets, an investor has to stick with their investments through market volatility and scary events. I think the PRP approach helps me to “stick with” my investments.

Market Crashes

There has been some significant volatility in the last 10 years. The PRP is not immune to volatility, but it generally had less volatility than being 100% invested in stocks.

Historical modelling shows me the typical and maximum drawdowns in the PRP. Sometimes, I have to remind myself that the maximum drawdown is -23%, which I haven’t experienced yet. It won’t be fun when it happens! Of course, the future may turn out even worse than historical back-tests.

The PRP is risky. Investing is risky.

Here’s a recap of the significant corrections / crashes in the last 10 years:

2020 pandemic: PRP had a -14% drawdown while

XBALhad a -21% drawdown. PRP did a great job during this market crash, with a significantly milder drawdown.2022 bear market: PRP had a -13% drawdown while

XBALhad a -16% drawdown. In this case, PRP showed only a slight advantage.2025 tariff surprise: PRP had a -6% drawdown while

XBALhad a -10% drawdown. This was a minor drop in both portfolios.2026 war: This drawdown is still in progress, but is currently no worse than last year’s. Like any drawdown, it could become much worse.

Evolution of the PRP

My portfolio started as the Permanent Portfolio (PP), and underwent a few changes along the way. When I re-designed it to apply the risk parity concept, I named my portfolio: Permanent Risk Parity (PRP).

- 2016: began as PP (25% stocks, 25% bonds, 25% gold, 25% cash)

- 2018: converted to PRP, with new weights (30/50/20)

- 2024: updated the allocations (40/40/20)

I made the 2018 change to apply a mathematically-derived weighting. The 2024 update increased the equity weight slightly, when I decided that I can handle a bit more equity risk. After the update, PRP now has virtually the same asset weights as the Golden Butterfly Portfolio.

Rebalancing Strategy

The portfolio is rebalanced once a year. This is largely done inside tax shelters to avoid triggering taxes. See recent example.

When I add (or withdraw) money, I look at the current asset weights, and make the transaction that would bring the portfolio closer to balance. Sometimes, this is enough to keep the portfolio balanced, without having to do the annual rebalancing.

For example, stocks are currently underweight at 38.7% of the portfolio. If I was adding new money today, I would buy stocks to bring them closer to the 40% target.

Portfolio Fees

The weighted average MER of my portfolio is just 0.14%, less than

the 0.20% MER of XBAL. In both cases, these are

rock-bottom fees.

I think it’s actually amazing that it’s possible to implement an

“alternative” investing technique like PRP at such a low fee. There

is a large industry of asset managers who offer complex and exotic

investment funds with very high fees. Many of these funds are not

any better than PRP (or XBAL).

— Jem Berkes